What Vice Chair Barr's Liquidity Speech Wasn't

His nonversation on liquidity got some analysts confused

Fed Vice Chair for Supervision Michael Barr gave a speech yesterday titled “Supporting Market Resilience and Financial Stability,” in which he talked about, among other things, some coming liquidity reforms from the Fed.

Most of what he discussed was not new. As he outlined in May, the Fed is considering:

Establishing a supervisory expectation of discount window readiness, inclusive of prepositioning collateral at the discount window such that the sum of lendable discount window collateral value + the bank’s reserves = some sufficient proportion of uninsured deposits.

Limiting banks’ inclusion of held-to-maturity assets in their calculations of regulatory liquidity ratios.

Ratcheting up liquidity regulations’ deposit outflow assumptions for some types of depositors.

And, broadly, revisiting the scope of liquidity regs for large banks. Presumably, this is about bringing more banks into the fold of the full LCR, etc.

(A previous Without Warning note discusses that speech, and particularly the shortcomings of the Fed’s designs for that third bullet point; see The Fed Is Hunting Bank Runners (May 30).)

In May, he said these were for banks “of a certain size.” Yesterday’s speech clarified marginally to say “community banks would not be covered, and we would take a tiered approach to the requirements.”

The non-update

In another section of the speech, however, Barr outlined a recent Fed update to its published FAQs on Regulation YY rules around banks’ internal liquidity stress tests (ILSTs). ILSTs are bank-run tests and are largely black boxes—i.e., not straightforward rules with published metrics à la the Liquidity Coverage Ratio (nor should they be).

Barr said the following (emphasis added):

We had been hearing that some were confused about how banks could incorporate ready access to the discount window and the SRF into their contingency funding plans and internal liquidity stress tests. Supervisors have a role in assessing the viability of large banks' plans to meet stressed outflows in their stress scenarios, and we have been asked whether the discount window, the SRF, and also Federal Home Loan Bank advances can play a role in those scenarios. The answer to this question is "yes."

We provided clarity to the public in August on permissible assumptions for how firms can incorporate the discount window and the SRF into their internal liquidity stress-test scenarios.

Some analyst coverage has interpreted this to mean the Fed has started giving banks credit in their ILSTs for assets prepositioned at the discount window/Standing Repo Facility.

That is not the case and, in any case, wouldn’t be that important given the assets included. Barr simply described what the August FAQ clarified, which was that banks’ ILSTs are allowed to assume that the discount window (and SRF and FHLBs) are viable monetization channels (only) for high-quality liquid assets (HQLA) in a stress scenario.

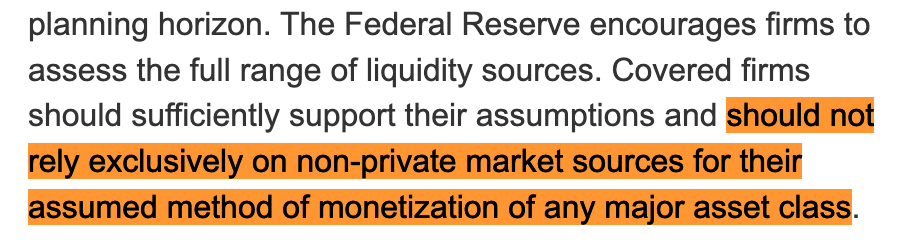

That is, banks with Treasuries and agency MBS sitting at (or at least nearby) the Fed can point to that as viable channel for monetizing those assets in a crisis. The FAQ specifically says that banks should not exclusively rely on these channels, however:

That is, a bank with all its Treasuries sitting at the Fed still can’t assume the Fed as a monetization channel for all those Treasuries in a stress scenario.

But this updated clarity is important for the banks that were hearing from some supervisors they couldn't use the SRF or discount window, even for Treasuries/etc, as part of their ILSTs—despite those being standing facilities. Anecdotal reports have suggested different banks were receiving different messaging (after all, Fed supervision spans 12 regional Reserve Banks) with regard to assuming access to the SRF/DW in liquidity tests.

But this is not a terribly meaningful change to the outcomes of these ILSTs, particularly in the cases where supervisors were already allowing it. The monetization value of USTs is likely similar whether at the Fed or in the market. There may be a slight numerator impact to the extent ILSTs were assuming higher haircuts on repos/sales of Treasuries in the private market during stress events; while the Fed will still rely on the securities’ market values at the discount window, it doesn’t raise haircuts in a crisis.

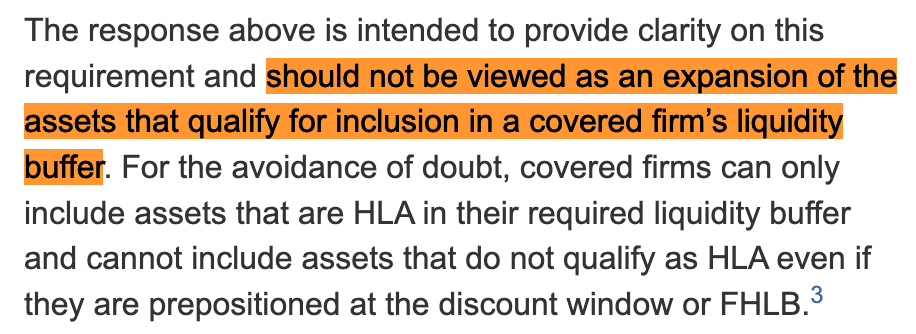

The updated FAQ specifically says this guidance is *not* an expansion of the assets that count towards a firm's liquidity:

And it underlines that HQLA (“HLA” in the excerpt above) still has to be HQLA. That is, the Fed has not assigned some liquidity value to any collateral held at the window. This change is not on the order of the Fed giving some “numerator” credit to a bank’s ILST for, say, a corporate loan that is pre-positioned at the Fed. The Fed has just clarified that banks can, in fact, assume they can take HQLA to the Fed in a stress scenario.

This FAQ update does nudge on a couple things:

It clarifies that banks’ ILSTs need not be able to also point to a different channel of monetization for things they plan to monetize at the Fed. This reduces some planning burden on proving access to additional funding sources that they do not intend to use. (It probably matters most for the SRF and FHLBs, given the stigma banks aim to avoid around the DW).

It improves the fungibility of reserves and Treasuries.

This was really the context in which Barr was discussing the FAQ change—as opposed to a change in discount window policy. As Barr put it,

We have heard over the years, however, that the degree of substitutability among these assets has been limited by concerns about capacity in stress for the market to turn securities into reserves immediately; these concerns are valid. This constraint can be addressed in part by the appropriate incorporation of Federal Reserve facilities into monetization plans in firms' internal liquidity stress tests.

The ILSTs, by rule, “must include an overnight planning horizon” among other time horizons. Monetizing HQLA at the Fed is a t+0 operation; whereas, private market channels may be t+1 (or longer), have certain time-of-day deadlines (which the SRF also has…), or have other administrative hurdles. If a Treasury is sitting at the Fed discount window, it can become reserves in an instant.

Thus, the FAQ clarification may help incentivize banks to shift their reserves demand into reserves/Treasuries demand—which may allow the Fed to shrink its portfolio further, at least in theory (non-bill Treasuries may be more imperfect substitutes with reserves).

Comments also welcome via email (steven.kelly@yale.edu) and Twitter (@StevenKelly49). View Without Warning in browser here.