Stablecoins' Ability to Meet Redemptions Is Not the Point

Also: There's no "flight to safety" on Planet Crypto, even with the safest stablecoins

A “crypto winter” is upon us, as markets have broadly fallen since late 2021. This month, a $19-billion algorithmic stablecoin imploded. But, in the aftermath, the headlines quickly shifted to Tether, the largest stablecoin in circulation. The value of tethers fell below their $1.00 peg on several exchanges. However, Tether said it honored all direct redemptions at $1, and its market price has more or less returned to par:

While the discussion tends to be around the safety of Tether’s and other stablecoins’ collateral and the ability to meet redemptions, this is a second order financial stability concern. (It’s certainly a consumer protection issue!) It’s the redemptions themselves that matter.

I wrote in Decrypt back in November that requiring non-bank stablecoins to safe-ify their collateral in lieu of becoming banks would risk a financial stability backfire. Take Tether. Let’s say we don’t like its reported bitcoin-backed loans and short-term corporate loan exposure in China, and we force it to hold cash or Treasuries. In practice, “cash” may mean an uninsured bank deposit, and “Treasuries” may actually mean Treasury repos with financial institutions.

For instance, here’s BUSD, Binance’s stablecoin (co-issued w/ Paxos) with a bit over $18 billion of market cap and holding the title of third largest stablecoin:

While stablecoins are pretty small yet, a large selloff these “safer” types of asset holdings would have much greater financial stability implications than a selloff of anything Tether might include in the “Other Investments (including digital tokens)” or “Corporate Bonds, Funds & Precious Metals” sections on its balance sheet.

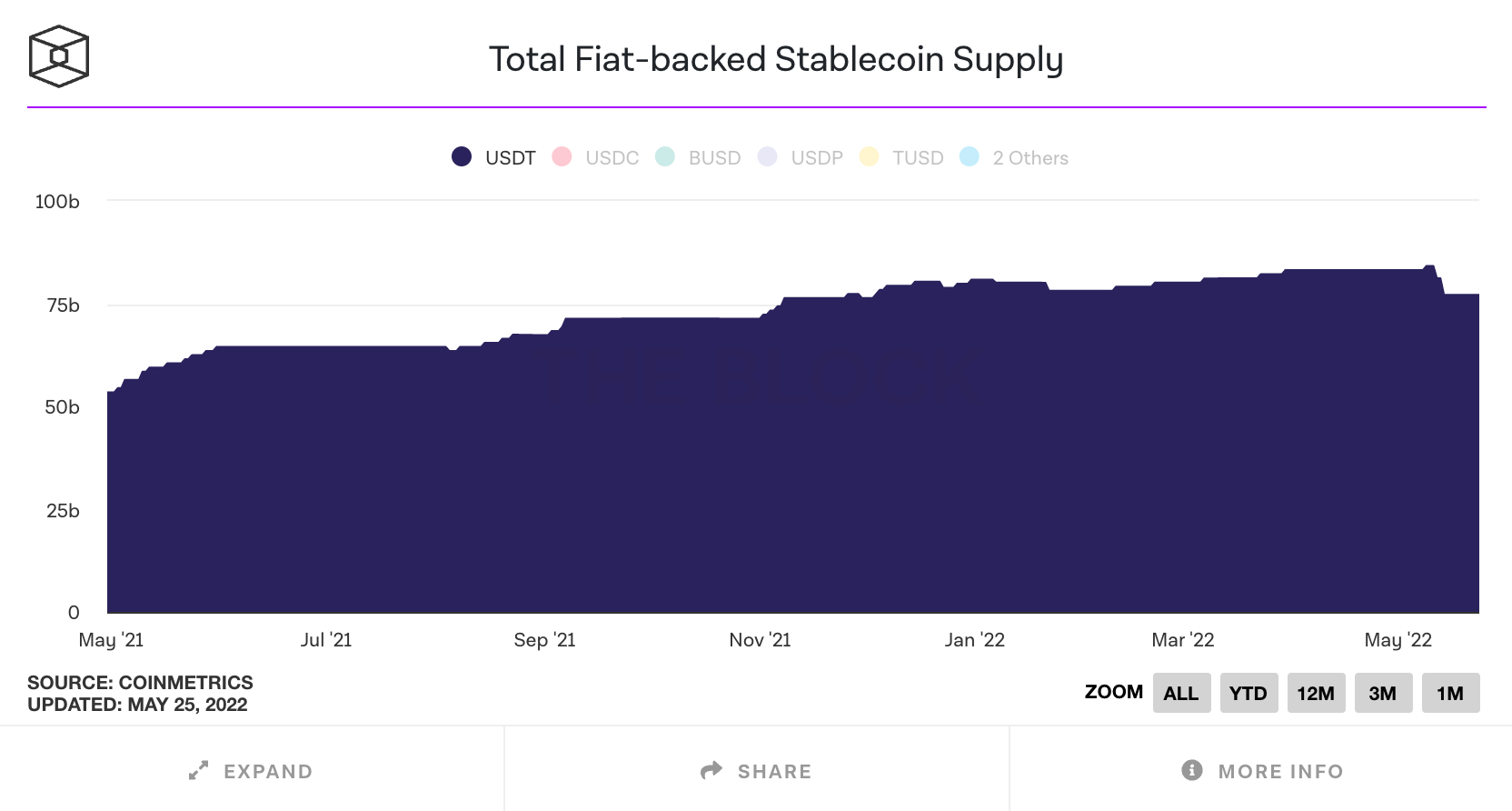

And it doesn’t take concern around a stablecoin’s safety for redemption to occur. As JP Koning has written, a lessened desire to transact in the crypto economy will naturally lead to less demand for the transaction medium of the cryptosphere: stablecoins. Excluding tether, the exit from fiat-backed (non-algo) stablecoins started around March of this year:

Tether’s market cap rose through March and then flattened, before falling as it met redemptions in the recent selloff:

But what about “flight to safety”??

A common pushback to the idea that stablecoins might provide a (the?) channel of infection from the cryptosphere to the traditional finance world has been a sort of “flight to safety” argument. The argument goes: Stablecoins won’t infect traditional finance’s money markets with crypto risks because crypto volatility would spur a run into stablecoins. That is, any risk-off sentiment amongst the likes of bitcoin and ether would only increase demand for the traditional banking system’s liabilities.

This is often how stablecoins are described in the media, and even by crypto traders themselves: a place to park your money when you want to exit your risky crypto investments, but not go through the time and cost to convert all the way back to fiat.

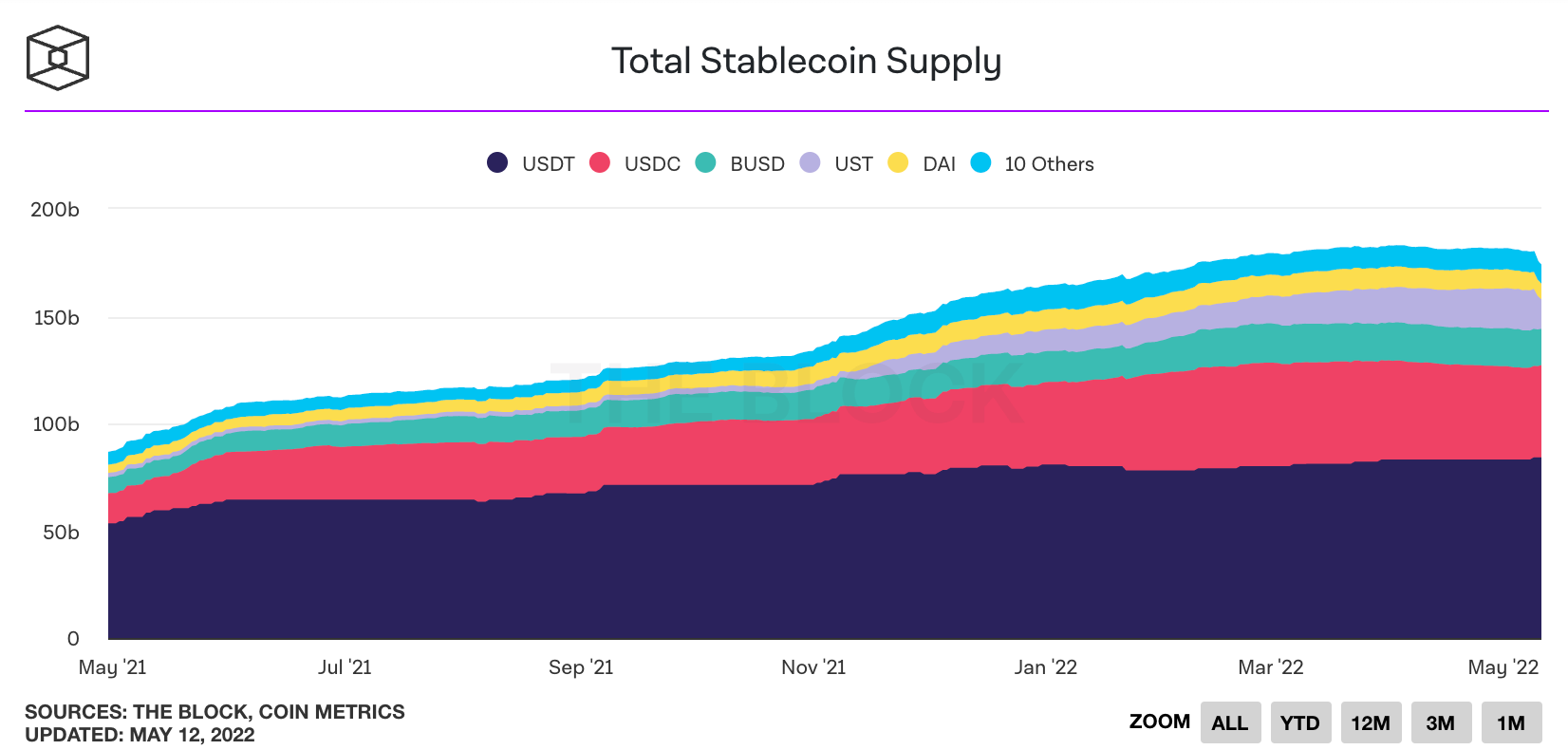

This narrative was only furthered when crypto markets began falling in late-2021 and stablecoin supply inflected to begin growing more sharply:

Market commentary and news coverage at the time referred to this as analogous to traditional finance investors moving to cash. Even crypto traders were being quoted as saying this was the market moving to the sidelines to wait for better investing opportunities.

This narrative that stablecoins are a sort of haven for traders to get out of risky coins without converting all the way back to bank dollars has persisted into the present sharp selloff. Here are a couple examples from core financial news sites in the aftermath of the Terra implosion and tether de-peg:

“Stablecoins are still mostly used by speculators, often as a place to park their money to avoid wild swings in crypto markets in lieu of regular dollars.”

“Stablecoins . . . play a central role in the stability of the broader crypto market by providing traders with a safe place to park their cash between making bets on volatile digital coins.”

“Crypto markets slumped today partly on worries about the future of Tether, where traders park their funds in times of high volatility . . .”

“Investors turn to stablecoins as a way of retaining value without leaving the digital asset ecosystem, acting as a safe haven from volatile coins or . . .”

But we’ve actually seen the supply of fiat-backed stablecoins, on net, fall in the latest month of crypto winter:

Some might have expected that any contraction in stablecoin supply from those exiting the crypto economy would be offset to some degree by those simply exiting their risky trades and “parking” their funds in stablecoins. Did that happen?

Nope. We witnessed no flight to safety—not this past month, nor when the stablecoin supply started growing faster back in November! Why? Stablecoins quite literally can’t actually serve that function…

In a market selloff in the traditional finance world, the first thing to adjust (as is the case in crypto) is, by definition, prices. The price has to fall enough for a buyer to take the asset off your hands, or for you to no longer be interested in selling. This can sometimes be enough for a selloff to end—i.e., the cure for a selloff is sometimes just a selloff. If a selloff continues, however, it will tend to move down the capital stack. A selloff that started in equities will infect junk bonds, then investment-grade credit, and so on until it ends.

But investors may run out of their existing liquidity, or may be unwilling to transact in a given market at any price. The “dash for cash” selloff may even extend all the way to the safest Treasury bonds (or it may even start there if that’s where the liquidity is). However, traditional finance has a central bank, which has two main levers here.

If the selloff extends all the way down to the safest assets, there’s a clear role for traditional monetary policy to intervene. If, say, U.S. Treasury bill rates are spiking, other money market rates will follow, and the Fed will step up and buy as part of its usual monetary policy implementation. Importantly, this expands the supply of “cash” available to investors. The central bank deposit-ified some assets. Secondly, there’s the discount window and any broader emergency discounting authority. These authorities allow central banks to directly monetize risky assets — again expanding the cash supply available to investors.

However, there is no stablecoin central bank. Which means the supply of the crypto “cash” is not elastic in this way. Sure, an individual can move out of Riskycoin and into Stablecoin, but that means someone else is taking the opposite leg. Stablecoins make for a nice medium of exchange, but the supply cannot expand flexibly to the risk-off developments of the cryptosphere. That is, the crypto market as a whole cannot move into stablecoins.

Aside from the small exceptions where Tether will mint tethers for a few favored counterparties against crypto collateral, new fiat needs to be onboarded for the stablecoin supply to be elastic. This works great when the demand for stablecoins is coming from outside the crypto economy (holders of fiat) — but doesn’t work at all when the demand is coming from across the cryptosphere (holders of risky crypto assets).

That is, for stablecoins to be a haven asset, they need new cash infusions during crypto market selloffs, and those injecting the cash need to want to swap out of their freshly minted stablecoins and catch the falling knife in bitcoin/ether/etc.

This also means that, rather than encouraging haven demand, all the (not infrequently dumb) things that lead to selloffs in crypto—celebrity tweets, algo ponzis’ music stopping, hacks, risk-off macro environments, etc.—can cause disruptions to systemically important funding markets, when they wouldn’t have if it weren’t for stablecoins.

Notably, if these non-bank stablecoins were turned into banks—as opposed to an intermediary interacting with the liabilities of banks, the supply of stablecoins would be flexible (because they would just be regulated deposits) and exiting to fiat wouldn’t require the extra step of selling off a giant portfolio of money market assets—or the bank asset portfolio the entity would be holding instead.

I’ve turned off the comments here, but they’re welcome and encouraged on Twitter or via email!