Checking in on the Main Street Lending Program

Loss accounting and the future of emergency liquidity for SMEs

All the Fed’s Section 13(3) emergency liquidity facilities have been closed for over a year, with the CARES-Act-supported facilities closed for over a year and a half. But, it wasn’t until last month that principal payments started coming due on the Main Street Lending Program (MSLP). And there’s a couple things worth checking in on.

As a refresher for what was now several market eons ago:

On April 9, 2020, the Fed announced its first design iteration of the MSLP, which targeted businesses that were too small to have access to public markets but too large to be assisted (or sufficiently assisted) by the PPP. The Fed later expanded the MSLP to also include nonprofits.

The MSLP purchased a 95% participation share in MSLP-compliant loans to small and medium-sized enterprises (SMEs) made by banks, and was available to hold up to an aggregate $600 billion—supported by a $75 billion equity injection from the Treasury, funded by the CARES Act through the Exchange Stabilization Fund (ESF). Designed to help ultimately viable businesses weather a period of disrupted cash flows, MSLP loans matured in five years and deferred interest payments for one year and principal payments for two. All MSLP-eligible loans carried an interest rate of LIBOR plus 300 basis points. In December 2020, Congress mandated the closure of the MSLP on January 8, 2021—after Treasury Secretary Mnuchin had already surprised the Fed in November in announcing it would close at year’s end. In total, the MSLP made $16.6 billion of purchases, its 95% share of $17.5 billion of MSLP lending.

And here’s a summary table of some main features of the design:

The Fed also netted about 50 bps in fees per loan. (And borrowers had additional fees.)

Interest Rates

Fees aside, the floating rate is notable given how much rates have changed relative to expectations at the time of the MSLP. Here’s the Fed’s dot plot from September 16, 2020:

With the fed funds target range at 2.25 - 2.5% and climbing, 1m LIBOR is around 2.4% and the 3m is at 2.9%—meaning MSLP borrowers are now paying 5.5% and climbing. But also, it’s not as if these are prime borrowers:

Plus, these MSLP borrowers may also be benefitting from the unexpectedly hot economy (relative to 2020) and/or have inflation-indexed income. Indeed, loss expectations are actually improving-ish. But the loss picture is a bit…weird.

Losses

Firstly: losses borne by the central bank observed ex post on its emergency lending are not a big deal. Full stop.

The Fed cannot ex ante expect losses on a given program that are greater than its level of subordinated protection—whether that protection be from Treasury, pooled borrower fees, Andreessen Horowitz, etc.

But a loss (observed ex post) on some transaction within an emergency crisis program might even be expected. (Though it’s true that none of the broad-based 13(3) programs in 2008 experienced a loss even at the transaction level.)

And so, in the event there’s a future MSLP, the experience of this one might be informative—and might constrain the Fed in designing one.

With the $75 billion in hand from the Treasury, the Fed set out some loss scenarios to get comfortable it was meeting its standard for “secured to the satisfaction” of reasonably expected repayment. It landed on permitting 8x leverage in the facility itself: $600 billion of lending.

As detailed by the Fed’s David Arseneau, et al. here, Fed staff projected bounds for the SPV’s net income under various credit risk scenarios and design choices, akin to a stress test. These scenarios utilized historical worst loan charge-off rates; projected loss rates from the Fed’s bank stress tests on non-investment grade, unsecured loans; and a credit rating agency’s default forecasts for the institutional leveraged loan market. The Fed considered multiples of these figures as well, ultimately weighing loss rates from approximately 5% to over 25%. Under the less adverse scenarios, including the worst historically observed commercial and industrial loan charge-off rate and the stress testing portfolio-average losses, the stress test projected that income would outweigh losses. The more adverse scenarios, however, were projected to cause losses.

With the covid recession ending quite rapidly, financial markets healing even more rapidly, and the labor market recovery being front-loaded, those dire outcomes were more than avoided:

MSLP and Losses

In its March 2021 monthly release on its emergency lending facilities, the Fed shared its quarterly update of the loss reserve on the facility—for an “as of” date of December 31, 2020. At this time, the Fed raised its expected loss rate on the loans from below 5% to over 14% without any listed explanation.

As of September 30, the MSLP had $2.2 billion outstanding, and a loss reserve of $96 million—a loss allowance of about 4.4%. On December 30, the MSLP had reached $16.6 billion and had a loss reserve of $2.4 billion—a 14.6% expected loss rate.

(Since then, the rate has stayed about this level on the outstanding loan balances. It’s currently 13.6%—$1.8 billion—on the $13.2 billion of loans still outstanding. However, this implies over $3 billion of principal paydowns and chargeoffs; only $32 million has been charged off, suggesting this has been mostly paydowns. If all of the $1.8 billion allowance materializes yet, the overall loss rate will fall to under 11%.)

This spike to 14.6% is a bit odd, as if there were a monstrous macroeconomic deterioration between September 30, 2020 and December 30, 2020—and one that has mostly lingered. There was a covid spike in late 2020, but it receded long ago and didn’t rewrite the the stronger-than-expected recovery story. Unemployment was over a percentage point lower in December 2020 than September 2020. As shown above, loss rates on similar loans stayed below 5% and have fallen below pre-pandemic levels.

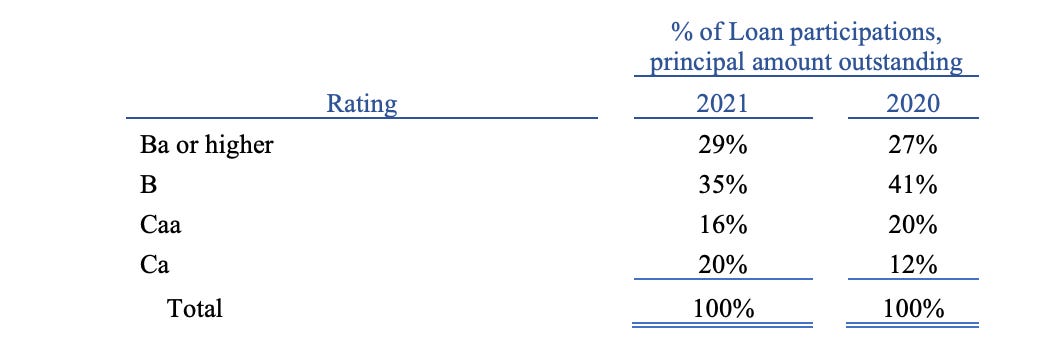

The only details offered on the MSLP’s relatively high expected loss rates were in the MSLP’s financial statements for 2020, which shared the following chart (circle added by me) showing a higher expected loss rate for service sector loans:

There was no mention of the increase from under 5%.

The Final Push

Participation accelerated into the MSLP’s close—just five months after opening for business (and two months after its final, most inclusive terms). Over half of the purchases were made in December. (This was variously attributed to rising covid cases, borrowers/lenders finally familiarizing themselves with the MSLP and becoming operational, as well as a final rush when the Treasury sprung on the Fed in November that Treasury would not authorize the facility past the end of the year.) As of September 30, the MSLP had $2.2 billion outstanding, and a loss reserve of $96 million—an expected loss rate of about 4.4%. On December 30, the MSLP had reached $16.6 billion and had a loss reserve of $2.4 billion—a 14.6% expected loss rate.

The terms did not become materially riskier in the final quarter; the October changes were just to encourage smaller dollar loans (only 12 of which were made below the previously in-force minimum).

The inspector general of the Fed’s Board of Governors said that, to handle the MSLP’s surge in volume in its final two months, the FRBB “implemented an expedited loan purchase process for certain lenders” and that the Office of Inspector General intended to assess this process.

In February 2021, the Congressional Oversight Commission (COC) wrote that in response to the surge in MSLP submissions in the program’s final weeks, “the FRBB increased staffing by bringing in additional trained legal and risk/compliance professionals from the [Fed] Board, the FRBB, and the [Federal Reserve Bank of New York], and the [MSLP] vendors also expanded the sizes of their teams considerably.” Additionally, both Fed and external staff added hours on weekends and evenings. Furthermore, the FRBB streamlined its loan review process during December by deferring review of items “that could be easily addressed on an ex-post basis” until after the acceptance of a loan. The FRBB initiated the streamlined approach for loans smaller than $5 million, expanding it as submissions increased to loans up to $50 million (excluding MSELF loans). The COC (no fan of the Fed) deemed the Fed’s process for buying and managing the MSLP portfolio “sufficient.”

I mention this just as something different about the final quarter of the MSLP’s life. None of this strikes me as particularly problematic, nor as obviously shifting the risk by 10 percentage points of loss allowance. (By contrast, it sounds like great, important work by Fed officials!) I have no idea what happened to affect the loss allowance so much.

A Quick Aside on Regulation A

The Fed’s “Reg A” rules are often confused with Section 13(3) statute, but they are the Fed’s implementing rules for liquidity provision, and the Fed will deviate from these principles (but never the statute) when not fit-for-purpose. (For more on this, see my Duke FinReg note here and the summary write-up of my conversation with Scott Alvarez, former Fed GC, here.)

The MSLP served as another reminder of this exceptionability. Section 13(3), as amended by Dodd-Frank, required that all recipients of Fed emergency liquidity be solvent. The law left it up to the Fed to make such a determination, other than stating:

A borrower shall be considered insolvent for purposes of this subparagraph, if the borrower is in bankruptcy, resolution under title II of the Dodd-Frank Wall Street Reform and Consumer Protection Act, or any other Federal or State insolvency proceeding.

Beyond that, it was the Fed’s call whether an entity was solvent. In addition to retaining discretion over whether an entity was insolvent, the Fed updated its Reg A to say that a borrower was “insolvent” if it was “generally not paying [its] undisputed debts as they become due during the 90 days preceding borrowing from the program.”

Makes sense.

The MSLP, however, granted a carveout from this. Its borrower certifications form noted:

For purposes of this certification, a Borrower has been “generally failing to pay undisputed debts as they become due” during the 90 days preceding the date hereof to the extent it is behind on its debts for reasons other than disruptions to its business resulting from the Coronavirus Disease 2019 (“COVID-19”) pandemic.

The form then offers a long “for the avoidance of doubt” section, noting the covid disruption could be on the cash flows side or on the financing side; it goes on to emphasize that the firm essentially just had to be current on their debts as of pre-pandemic.

Again, makes sense. It would be silly to create a program designed to assist firms with financing problems due to the pandemic and then exclude firms with pandemic-induced financing problems… Moreover, the MSLP did not become operational until July 6, 2020—over 90 days into the pandemic. Sensible use of Reg A’s flexibility.

A Future MSLP

We know for sure that any future MSLP won’t be identical to the covid-era one. The “Consolidated Appropriations Act, 2021,” passed in December of 2020, prevented the Treasury from using ESF funds for any Fed program that is “the same as” the MSLP (or the same as the muni or corporate bond facilities). But, assuming the Fed can navigate that language (which applies only to the Treasury’s ESF), the loss ratio above raises some important questions.

For one, the facility was capitalized by Treasury at a rate of 12.5% ($75 billion of equity for $600 billion of lending). To be sure, the facility also capitalizes itself further with fees and interest income. (So far it’s accrued $900 million.) Still, a loss allowance like the one the Fed’s recorded since December 2020 raises eyebrows, especially on a go-forward basis if a similar program in the future has to decide its ex ante expectation of loss rates.

A direct lending program to mid-sized businesses is one that probably should eat through its capital. Given that it’s not a market-based program, and the debts are very heterogenous, there is likely not much by way of an “announcement effect.” The proof of the pudding is in the lending.

Yet, we did not see the tail risk scenarios play out that the Fed had sketched out, and still the expected loss rate bumped up by 10 pps. Even if the Fed and Treasury are in agreement that the Treasury capital (or whomever’s capital) should evaporate, the Fed is legally obligated to expect repayment even in (reasonable) downside scenarios—not just in the scenario of the two-month recession, sharp recovery, and loan default rates less than in 2014…

Thus, without substantial additional context on what’s driving that loss rate, we might expect there to be a greater legal hurdle in the future for any such SME lending. (Not that the Fed is exactly champing at the bit to roll it out again…)

PS: A Weird Thing

The TALF, MLF, PPPLF, and MSLP all still have non-zero balances and are operating in runoff mode. As noted above, all have been closed to new activity for a long while. The Fed still publishes transaction-level updates every month on the first three . . . but not on the MSLP. It says:

The MSLP ceased purchasing participations on January 8, 2021; therefore, the Board will not provide additional transaction-specific disclosures about the MSLP on a periodic basis going forward.

Okay fine. The Fed is still meeting its disclosure obligations on the MSLP under Section 13(3) and under the CARES Act. And it met its Section 11(s) disclosure obligation (which was no different than what it had already been disclosing), over a year ago. (And I’m sort of ambivalent about emergency lending disclosures anyways given the tradeoffs inherent in them.) But, like, what’s the deal with the Fed’s justification? It similarly has stopped purchases under the other three facilities, yet we still get those disclosures. What’s the difference? Hmmm.

The upshot of this whole post: I’m not sure what’s going on. Without Warning will always be free.

Comments are turned off here but more than welcome via email (steven.kelly@yale.edu) and Twitter (@StevenKelly49).